Simulate VAR model

This function can (and should) be used to generate a VAR process of any order.

simulateVAR(N = 100, p = 1, nobs = 250, rho = 0.5, sparsity = 0.05, mu = 0, method = "normal", covariance = "Toeplitz")where the parameters are

-

N: the dimension of the VAR model (defaultN = 100); -

p: the order of the VAR model (defaultp = 1); -

nobs: the number of observation for the series (defaultnobs = 250); -

rho: the intensity of the variance/covariance matrix; -

sparsity: the percentage of non-zero elements in every matrix of the model (defaultsparsity = 0.05); -

mu: an N vector for the mean of the process (defaultmu = 0); -

method: the distribution used to generate the non-zero entries for the matrices of the VAR. Possible values arenormal, bimodal(defaultmethod = "normal"); -

covariance: the type of variance/covariance matrix for the process. Possible values are:block1, block2, Toeplitz, Wishart, diagonal(defaultcovariance = "Toeplitz").

The output of the command

sim <- simulateVAR()is an S3 object (or, if you want, a list), with attr(*, "class") = "var" and attr(*, "type") = "simulation", containing the following elements:

-

A: it is a list ofpsquare matrices of dimensionN; -

series: annobs x Nmatrix containing the simulated series; -

sigma: the variance/covariance matrix of the process; -

noises: thenobs x Nmatrix of the errors.

In the following we will see how to create a (random) VAR model that can be used for testing pourposes.

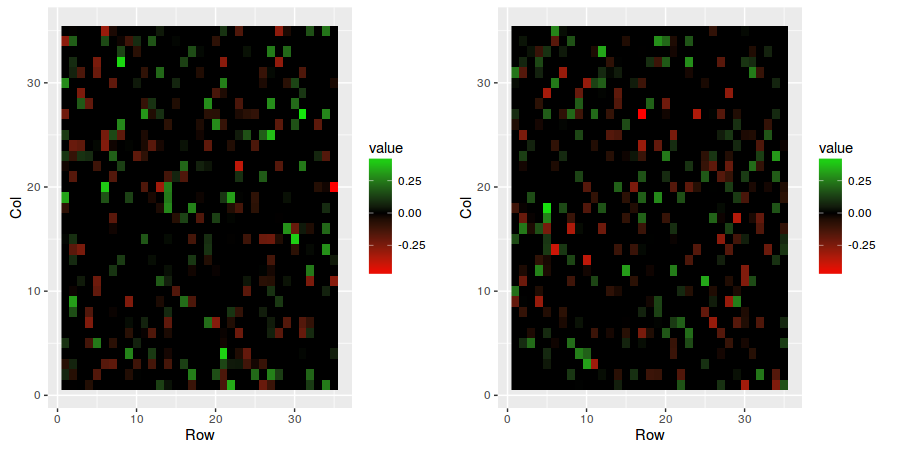

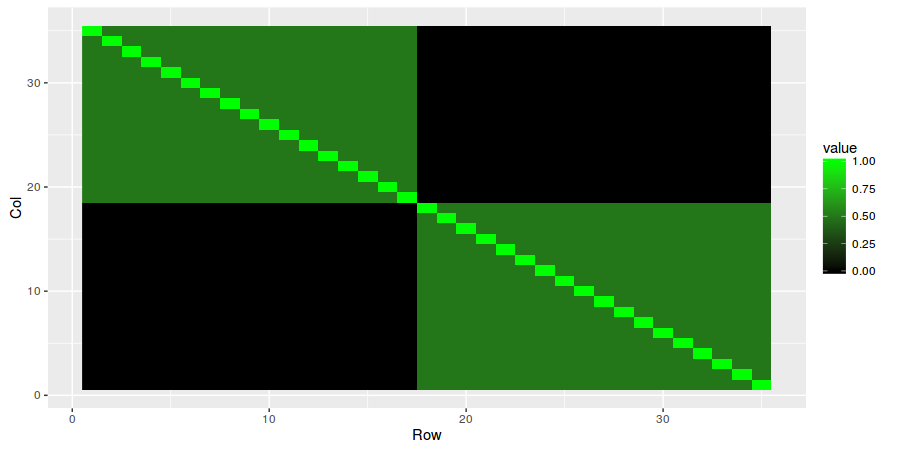

First we initialize the random seed to 0 and then we create a VAR(2) model with dimension N = 35, sparsity = 0.25 and covariance = "block2".

set.seed(0)

sim <- simulateVAR(N = 35, p = 2, sparsity = 0.25, covariance = "block2")To see the results, simply plot the VAR matrices and the variance/covariance matrix.

plotVAR(sim)

plotMatrix(sim$sigma)